Australian pro AV market: Enabled by scale and solution diversity

Australia’s share (1.4%) of the global professional pro AV market of $325 billion (A$484.5 billion) approximately matches its share of global GDP of 1.6%. But the low share belies a large market enabled by a GDP of 1.72 trillion USD (A$2.56 trillion).

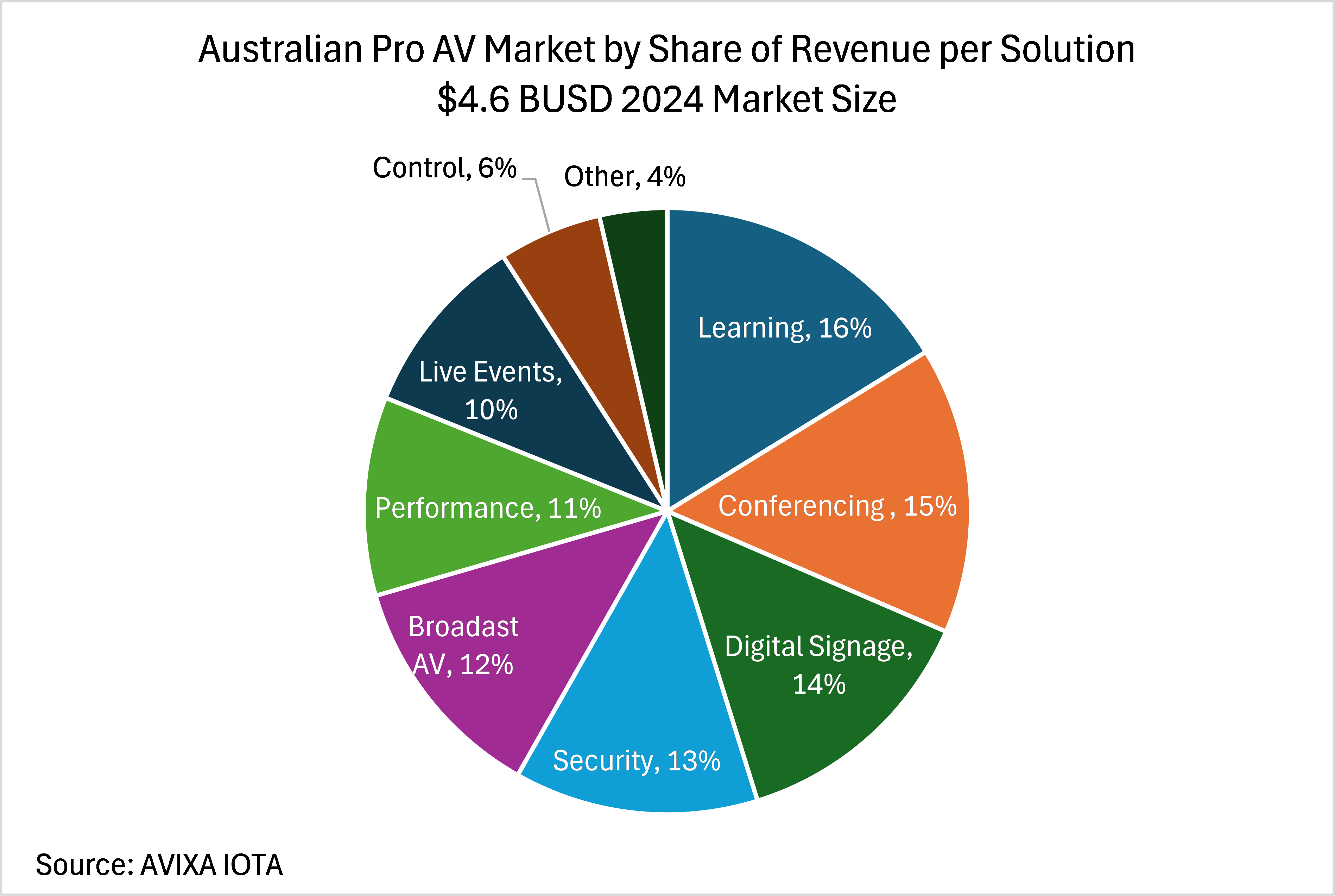

According to AVIXA’s 2024 Industry Outlook and Trends Analysis (IOTA), the Australian market will end 2024 at $4.6 billion USD (A$6.8 billion), with 5.4% growth over 2023, on its way to becoming a $5.9 billion USD (A$8.79 billion) market in 2025. The pro AV market leverages the country’s scale and solution diversity to grow business.

ADVERTISEMENT

Australia has the unique characteristic of having most manufacturers of pro AV products located in other regions. In addition, with few national integrators, the market is largely comprised of hundreds of small integrators pursuing sub-categories, often along vertical lines, such as education, commercial or government/defence. Within the verticals, the largest solutions segments, according to AVIXA’s IOTA, are learning, conferencing and collaboration, digital signage, security/surveillance, and life safety and broadcast AV.

It is noteworthy that no single solution dominates the market, which allows room for a wide variety of products and services across the integrator landscape. For example, in the corporate sector, product segments include content management hardware, capture and production equipment, control and collaboration systems, video displays, audio equipment and infrastructure.

Another factor is the market’s high transport costs since most goods need to be brought in from outside. These transport costs add to the pricing challenges of the market, which is already competing with low-cost goods from China.

Recent economic pressures, such as higher interest rates, global economic uncertainty and persistent inflation have placed added challenges on the Australian pro AV industry in 2024. These factors are the latest concerns for an industry just a few years past the pandemic, in which the market faced similar challenges as elsewhere, namely, the loss of live events and supply chain shortages.

In the aftermath, while live events are coming back, the office market has been hit by the work-at-home and hybrid office trends. For example, Australian employers expect employees to work at home at least 1.6 times a week, according to WFH Research. Additionally, in mid-2024, office vacancy rates rose above 10% in Sydney, Melbourne and Perth, where most of the large companies have their headquarters, according to the Property Council of Australia. While near recessionary 1990 levels, the vacancy rate is substantially less than the 20% experienced by many U.S. cities due to the transition to hybrid work.

The transition to the hybrid office is also happening during economic headwinds that have seen company insolvencies increase to higher levels than last year, according to the Australian Securities and Investments Commission.

As in other markets under similar pressure, pro AV buyers are seeking cost-efficient solutions that match the flexibility of the new office environment, namely software platforms are favoured over traditional conferencing and collaboration hardware. According to AVIXA’s IOTA, Australian pro AV buyers will spend $165 million (A$246 million) on standalone software in 2024, more than 20% of it on conferencing and collaboration solutions.

More promising than the corporate market are the performance, entertainment and live events segments, which have returned to a full slate of performances in 2024 and are likely to continue expanding right through the 2032 Brisbane Summer Olympics. At $940 million (A$1.4 billion) in 2024, the solution areas comprise more than 20% of pro AV spend and serve as contributors to other solution areas such as broadcast AV for content development and digital signage for event displays.

Learning, the largest single market at $752 million (A$1.1 billion) reflects the significant investment Australia makes in education, particularly through the national government, which recently designated an A$24 billion multi-year grant for education projects. Though the solution suite for education is similar to the commercial sector, a greater amount of the investment is allocated to video displays and projection, capture and production equipment and audio equipment to outfit classrooms and labs with the latest interactive capabilities.

A remaining issue for the Australian market has been the lack of trained pro AV professionals, many of whom left the country and/or the profession to seek other roles during the pandemic. But training programs, such as AVIXA’s Certified Technology Specialist (CTS) can help bring new professionals into the market.

Overall, though challenged by the economy and changes to the commercial market, Australia’s pro AV market is expected to carry on enabled by the return of events and education projects, while adding an ever-growing staff of new professionals.

This article was written by AVIXA senior analyst Mike Sullivan-Trainor.

-

ADVERTISEMENT

-

ADVERTISEMENT

-

ADVERTISEMENT

-

ADVERTISEMENT